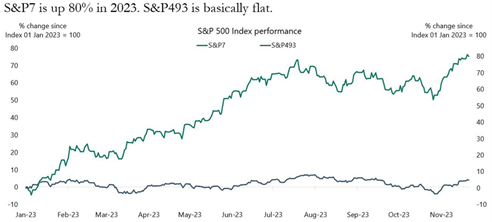

The top 7 stocks in the US, now called the ‘Magnificent 7’, accounted for nearly all the gains in the S&P 500 in 2023. When we plot the top 7 stocks in the S&P 500 against the remaining 493 stocks for the year, you can see the outperformance of these top names. Essentially, anyone not in the top 7 names underperformed. The question is ‘’will this outperformance continue?’’

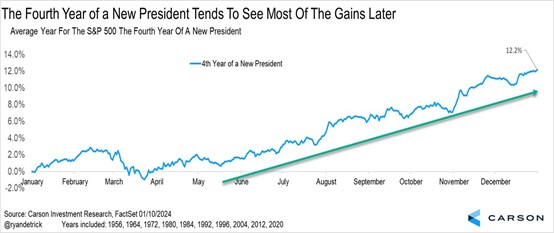

Source: @RyanDetrick via X.com

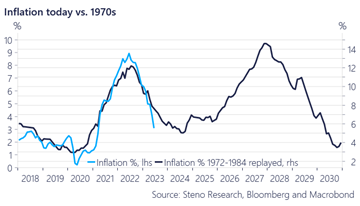

The main risk to equity markets in 2024 is likely to be a rebound in inflation. The following chart shows the waves of inflation seen in the 1970’s, and the pattern is surprisingly similar at this stage. History has a way of rhyming, although right now we are not seeing any sign of the 2nd surge.